Olympia, WA — A temporary rule designed to protect consumers from being charged higher insurance rates is being challenged in court.

In March, Washington’s Insurance Commissioner filed an emergency rule that took the industry by surprise: a ban on the use of credit scores to set insurance rates.

In a lawsuit filed today, the American Property Casualty Insurance Association (APCIA) says Washington’s Insurance Commissioner doesn’t have the legal authority to issue the ban.

“Commissioner Kreidler is attempting to prohibit an important risk-based rating tool that has been in place for nearly 20 years for the benefit of consumers. The Commissioner is attempting to circumvent the Washington Legislature by taking an action the Legislature recently explicitly rejected,” says APCIA general counsel Claire Howard.

In the filing, she notes the emergency rule went into effect just two weeks after the state Senate failed to vote on SB 5010 before a key deadline. The bill, supported by Kreidler and Governor Jay Inslee, would have rewritten the law to ban using credit scores as an insurance factor permanently.

Commissioner Kriedler says he’s ready to defend the temporary rule and believes the Coronavirus pandemic gives him the emergency powers necessary to act on behalf of consumers.

“What it’s doing to people of lower income, or people of color because of the financial challenges - it’s clear that I have the authority to protect people under those circumstances,” says Kreidler.

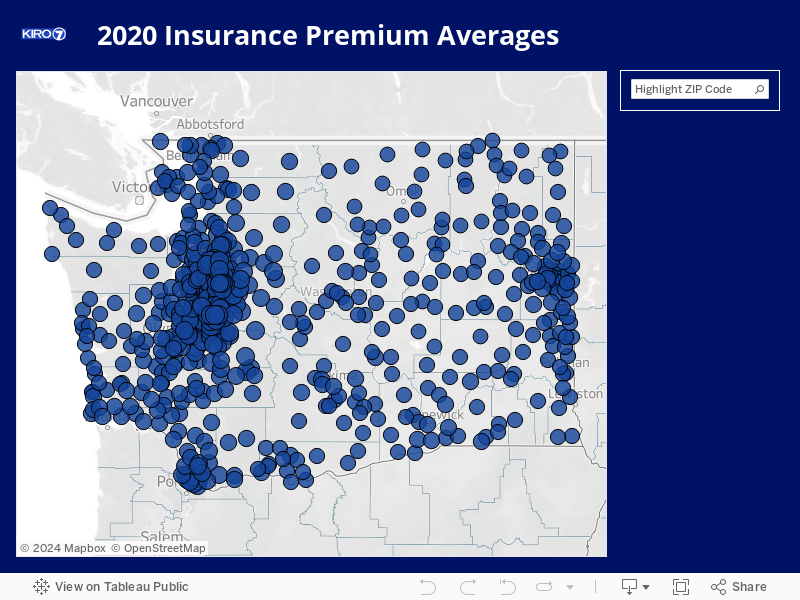

KIRO 7′s Jesse Jones has been investigating how credit scores factor into insurance rates for months. A study from the Consumer Federation found that drivers with low credit scores and perfect driving records can pay up to 79 percent more for insurance than drivers with excellent credit, in a state minimum policy.

We created this map, based on insurance industry data and a Consumer Federation study, to see what average rates for poor, fair, and excellent credit scores may be.

See our previous reporting here:

- Emergency rule temporarily bans credit scoring to set insurance rates

- Bill to take credit scoring out of insurance rates dies in the Senate

- Seattle NAACP among dozens of groups now supporting full ban on credit scoring in insurance

- Insurance industry helped write changes that regulator says ‘gutted’ bill to take credit scoring out of insurance

- Race, credit scoring, and the most expensive neighborhood for car insurance in Washington

Email Jesse right now at consumer@kiro7.com

Cox Media Group