Olympia, WA — Washington’s Insurance Commissioner just issued an emergency rule that keeps insurance companies from using your credit score to set rates. It’s a stunning development that will impact many of you who are paying more.

Commissioner Mike Kreidler’s action caught the industry by surprise.

“This is one where we have a chance to make a substantial difference to protect people so they’re not being harmed by an arbitrary rule,” says Kreidler.

Kreidler is using the CARES Act as the key to start his temporary emergency rule.

See, under The CARES Act not all negative reporting is placed on your credit report. Because of that, Kreidler believes credit bureaus are collecting inaccurate information.

And since the insurance industry uses the scores to help determine rates, he’s calling these scoring models unreliable.

“We’re very sensitive to the people who are being harmed. Let’s get this out there before any more people are hurt,” says Kreidler.

Reaction from the insurance industry

Kenton Brine is with the NW Insurance Council, a trade group that represents some of the biggest insurers in the country.

“Overall, I’d say we’re stunned and disappointed that the commissioner has chosen this route,” says Brine.

He believes the emergency rule will hurt consumers.

“There’s a high risk that the price of insurance will be going up because credit scores have been shown to be a way in which insurers can help reduce the cost of insurance for consumers,” says Brine.

Here’s what our reporting finds

We’ve been investigating insurers’ use of credit scores for three months.

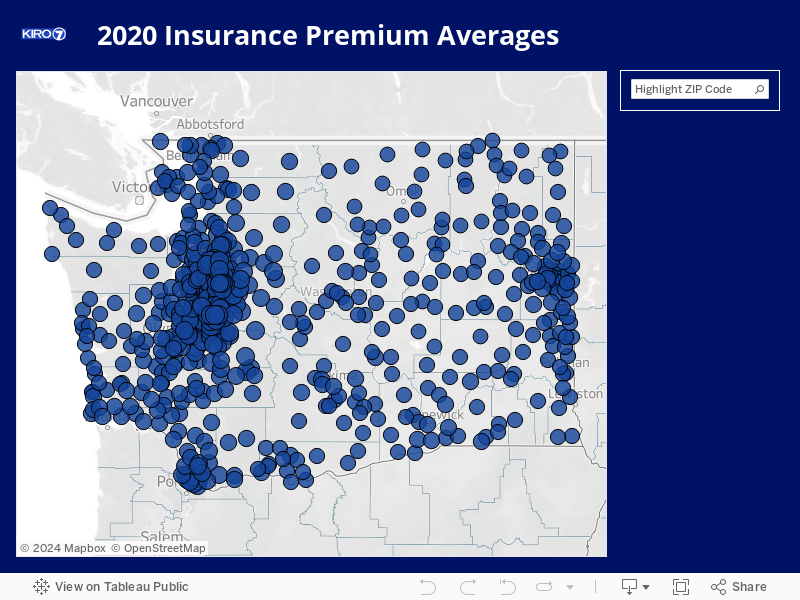

We spoke to experts at the Consumer Federation conducted a study of insurance rates. Their data show Washington drivers with poor credit and a perfect driving record can pay up to 79% more than a driver with excellent credit in state minimum policy.

You can use this interactive map to see what the study shows average rates may be in your area.

Support for taking credit scoring out

“And so when you punish drivers with perfect driving histories but less than perfect credit, the insurance companies make coverage more expensive for those least able to afford it,” says Consumer Federation insurance expert Douglas Heller.

A Federal Trade Commission Report says that 26 percent of Blacks have the lowest 10 percent of credit-based insurance scores - a number which combines credit score and other factors to set rates for a policyholder.

“Some have just relied almost excessively - 60, 70 percent of their underwriting - on use of credit,” says Insurance Commissioner Mike Kreidler.

In our reporting, we also analyzed rate and census data and found that the zip codes with the highest percentage of blacks pay some of the highest auto insurance rates in the state.

You can see that plotted out on this map and this scatterplot.

Gerald Hankerson from the Seattle-King County NAACP says Kreidler’s action was necessary.

“Finally, someone had the courage to do something the legislature couldn’t be able to do. How long were we supposed to allow this discriminatory practice to continue before somebody stepped up? So we applaud Commissioner Kreidler for doing what he did,” says Hankerson.

A political policy battle

Earlier this year, Senate Bill 5010 was introduced in Olympia to end the use of credit scores by insurers. The bill was later substituted to a three year credit score freeze for insurance purposes instead.

The legislation passed committee but never made it to the floor for a vote.

“In my nine years I’ve never seen an agency head run a bill through the legislative process and then if that bill didn’t pass, I’ve never seen somebody just enact it kind of through fiat power. It’s really bizarre,” says Senator Mark Mullet, chair of the Senate Financial Institutions, Economic Development & Trade Committee where SB 5010 was debated.

Kreidler tells me rates don’t have to go up. He says insurers can figure it out by going old school.

“What’s their driving record? Golly, that’s really rocket science isn’t it. You have to look and see what people are doing when they’re behind the wheel as opposed to just taking a look at a credit score and drawing up broad assumptions,” says Kreidler.

The Commissioner says this rule will stay in place 120 days. And expects it to be extended while in the rule making process.

Kreidler’s office says the changes could last for as many three years.

Read more of our reporting on this process here:

- Bill to take credit scoring out of insurance rates dies in the Senate

- Seattle NAACP among dozens of groups now supporting full ban on credit scoring in insurance

- Governor speaks out in support of ban on use of credit scores to set insurance rates

- Insurance industry helped write changes that regulator says ‘gutted’ bill to take credit scoring out of insurance

- Bill to end use of credit scoring in insurance rates may get a vote - with major changes

- Race, credit scoring, and the most expensive neighborhood for car insurance in Washington

- Could you pay less for insurance, under a proposal to ban using credit scores to calculate premiums?

Email Jesse right now at consumer@kiro7.com

Cox Media Group