Seattle, WA — When Theo Martin drives from his home in Seattle’s Central District to his restaurant in Columbia City, he’s commuting between two zip codes: 98144 and 98118. The pair have some of the highest car insurance rates in the state.

“A shock. To know that where I work and where I live has the first and the fourth highest insurance for automobiles. And I have five of them in our family,” says Martin.

Also - those zip codes have the area’s largest percentages of black residents.

“This is where I was raised, this is my home,” says Martin. “I want to stay here. I would like to know why I am paying more for my insurance.”

The main reason for that, according to Insurance Commissioner Mike Kreidler, is the insurance industry’s use of credit scoring to determine auto rates.

I had to ask him: do you believe that the use of credit scoring for insurance rates is racist?

“Yeah, I do,” Kreidler replied.

Kreidler says most of those with low credit scores are also low-income. Up to 60 percent of what you pay is determined by your score.

“Disproportionately represented in lower income are people of color. It’s a manifestation of our society,” says Kreidler.

And a report from the Federal Trade Commission Report bears that out, saying 26% of Blacks have the lowest 10% of credit-based insurance scores.

We also checked data provided to us by the Consumer Federation of America (CFA), obtained from Quadrant Information Services, LLC. Quadrant provides pricing analysis for insurance companies and crunched data using insurance companies’ algorithms filed with the state.

The study used a 35-year-old unmarried driver licensed for 19 years with a clean record, who drives a 2011 Honda Civic LX 12,000 miles a year with state minimum liability coverage. The data looked at differences in credit score and gender.

“We have over 37,000 quotes for drivers in the state of Washington to arrive at our conclusions here,” says CFA insurance expert Douglas Heller.

The Consumer Federation says in Washington state, drivers with poor credit shell out 79% more on average than drivers with excellent credit.

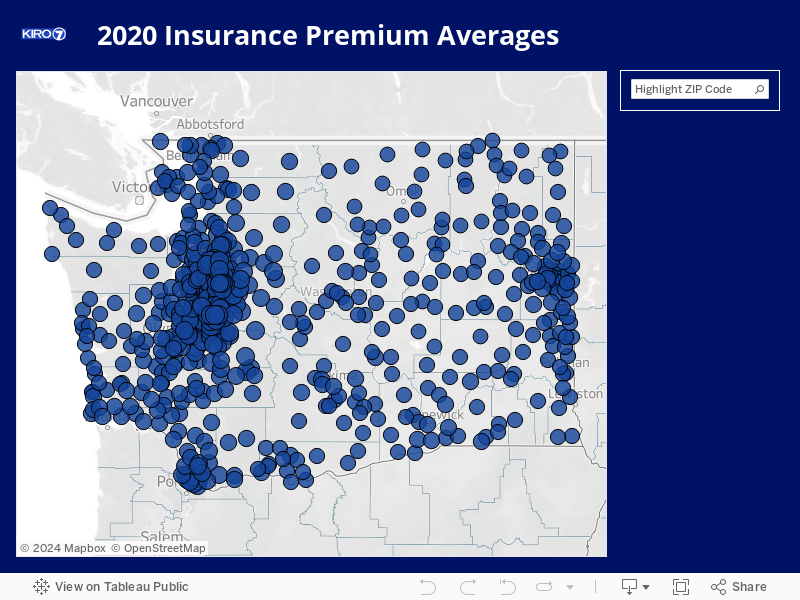

See for yourself: use this map to see average insurance premiums across the state. To search for your zip code, use the search box in the right-hand corner.

Like Kreidler, Heller believes using credit scoring disproportionately impacts communities of color.

“There is a long history of systemic bias in access to financial services in America. And, as a result, people of color - on average - have lower credit scores than white Americans,” says Heller.

Theo Martin’s parents, Loy and Lula Martin, moved to Seattle in the 1940s.

And he says redlining - legal restrictions that banned blacks from buying or renting in certain areas - forced them to live in the Central District.

“I would say the Central District - where I was raised - was called the ‘colored district.’ I didn’t know it meant Central District. I just thought CD was because it was full of colored people,” remembers Martin.

Shaun Scott from the Statewide Poverty Network says those restrictive covenants and decades of systemic racism put Blacks behind economically.

“So if you were barred or denied the ability to climb that ladder because you were denied access to home ownership, with the history of racially restrictive covenants in the state of Washington, zoning laws that bar renters from taking up occupancy in most of the city - that’s going to impact your socioeconomic standing,” says Scott. “Not just in your own lifetime, but in the lifetime of those that come after you.”

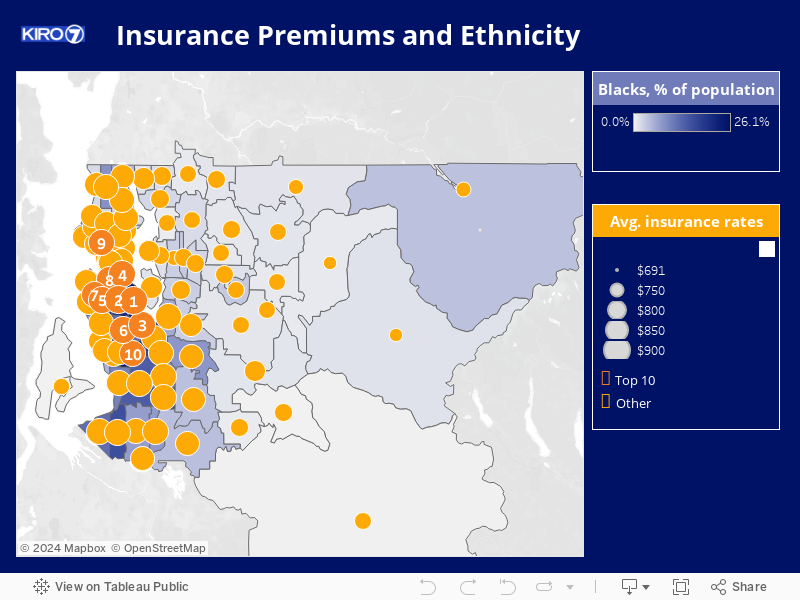

Let’s map this out with the help of Tableau.

This visualization shows King County. The areas in blue have been shaded to show the highest percentages of black residents. Now let’s see the zip codes where the highest auto insurance rates are.

And four of these, according to the study, have the four highest average rates in the state:

- 98118 - in the Rainier Valley,

- 98108 and 98144 - which include Beacon Hill, South Park, Leschi, and the Central district

- 98178 - in Skyway

Let’s try this another way. This scatterplot graph shows the average premium for poor, fair, and excellent credit scores in neighborhoods by percentage of Black population. It’s not a perfect match, but there’s a correlation. The numbers tend to go up.

Commissioner Kreidler says these findings are the results of a societal wreck at the intersection of race and economics.

“This is something wrong in our society that should have been changed. This should never have been allowed to ever get off the ground,” says Kreidler.

Kenton Brine with the Northwest Insurance Council says he’s not buying this data or its conclusions.

“If you look at specific zip code areas, there are other differences as well that have nothing to do with race or income. There may be more accidents per capita in that part of, in that zip code area. Or there might be higher auto theft rates,” says Brine.

What about a driver’s record?

“Driving records can be notoriously inaccurate. And, in fact, they can have racial bias as well. Studies show from the Standard Policing Project study that black drivers are 20 percent more likely to be pulled over than white drivers, and they’re more likely to be cited when they are pulled over,” says Brine.

Hold on. The insurance industry appears to admit there’s systemic racism in policing to make its argument that there’s no systemic racism in insurance rates.

There’s a bill in the legislature - Senate Bill 5010 - that, if passed, would ban the use of credit scores. Brine says a similar law in Alaska hit consumers hard.

“And a large segment - like 40 percent of consumers in Alaska - saw rate increases because that factor was removed,” says Brine.

But Commissioner Kreidler says California also banned using credit scores and prices didn’t go up.

“You didn’t see change. When they started introducing it, when they started introducing credit scoring nationally, California didn’t permit it from day one,” points out Kreidler.

As for Theo Martin, all he wants is to be provided the opportunity to be judged by acts - not algorithms.

“Judge me by what I do, not by how I pay. Not by my credit report,” says Martin. “It should be equal across the state. All of us should get rated on our driving.”

SB 5010 still hasn’t been scheduled for a vote. And the deadline for it to pass out of committee or die on the vine is February 15. As we were getting ready to air this story, we were told the committee chair is planning to meet with the Office of Insurance Commissioner to see whether they can come to a compromise that gets the bill to a vote.

Special thanks to: Tableau and the Seattle Civil Rights & Labor History Project at the University of Washington, including Anna Yoon, Brian Lam, Gihoon Du, Jiang Wu, and Yurika Harada.

Email Jesse right now at consumer@kiro7.com

Cox Media Group