Olympia, WA — The NAACP and other community groups are now pushing to end the use of credit scores to help determine insurance rates.

“This is nothing more than the Jim Crow-era tactics they used against the disenfranchised and marginalized people to make them pay more hoping they default,” says Gerald Hankerson, president of both the Seattle-King County NAACP and its larger regional conference.

Hankerson says the insurance industry’s use of credit scores is no different than redlining - the now-illegal practice of charging people of color more to rent or buy homes, or preventing them from living in certain areas altogether. Red lining restricted communities to certain neighborhoods and was stopped, beginning in the late 1960s.

“I call it modern-day red lining because that’s essentially what it does. We can’t find the link between credit scores and driving records that allows poorer people to have a higher premium than non poor people,” says Hankerson.

We’ve been investigating the use of insurance scores to determine insurance rates for months.

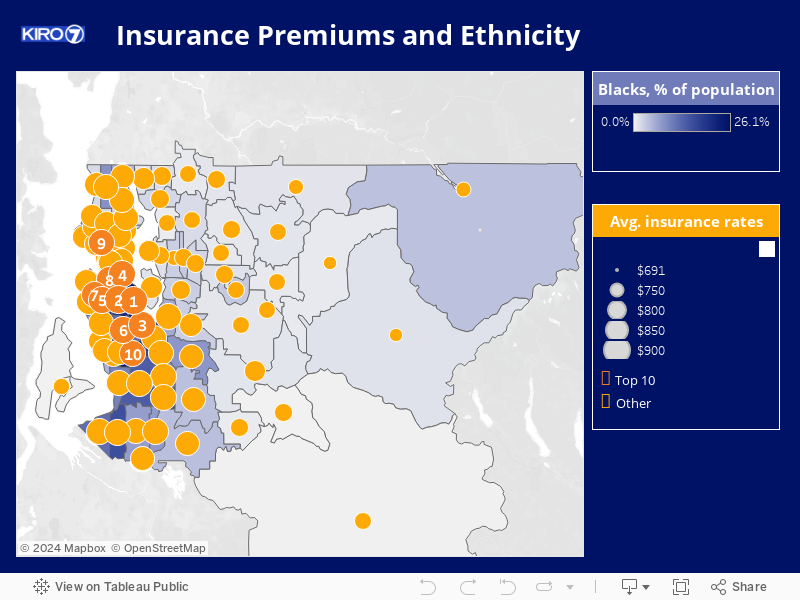

Our investigation found a Federal Trade Commission report shows that 26% of Blacks have the lowest 10% of credit-based insurance scores.

We also ran the numbers and found that zip codes with the highest percentage of blacks have among the highest auto insurance rates in the state. See it mapped out here and here.

“But if the poorest people are paying the highest premium and the richest people are not , how is it not racist?” says Hankerson. “Unless you are punishing poverty which is essentially racist all the same.”

Senate Bill 5010 was written this session to ban insurance companies from using credit scoring.

However, State Senator Mark Mullet, who’s the chairman of the Senate Business, Financial Services & Trade Committee, pushed a substitute bill that allows credit scores, but would freeze them for three years.

The changes were written, at least in part, by an insurance company employee.

“For the next three years your score can go up but it can’t go backwards. And we’re buying some time for, hopefully to continue to look at this policy,” said Mullet.

Just last week Governor Inslee said the bill needs to go back to its original form.

“So we’re urging the legislature to take another crack at this and bring this back to what the state needs. Which is a strong stand against a discriminatory practice in this very important industry,” said Inslee.

At least 35 community groups, including the AARP of Washington, Catholic Community Services, and the Washington State Labor Council - along with the NAACP - have signed letters asking for the original bill to be passed.

26% of African Americans are in the group with the lowest 10% of credit-based insurance scores, while only 3% are in the highest 10% of scores. Similarly, 19% of Hispanics are in the group with the lowest 10% of scores, and 5% are in the highest 10% of scores.

— Federal Trade Commission report

State Senator Mona Das authored the original bill.

“I know this bill was watered down, I know this bill, the amendment was mostly written by the insurance companies who have been making a lot of money on the backs of marginalized communities and folks with low income and particularly low credit scores,” says Das.

Senator Das would like to see the bill back in its original form. But it has to live first.

“There’s no way to negotiate a dead bill,” says Das. “So if it doesn’t leave the committee there’s no more conversation.”

The deadline for bills to be voted out of their house of origins is Tuesday March 9.

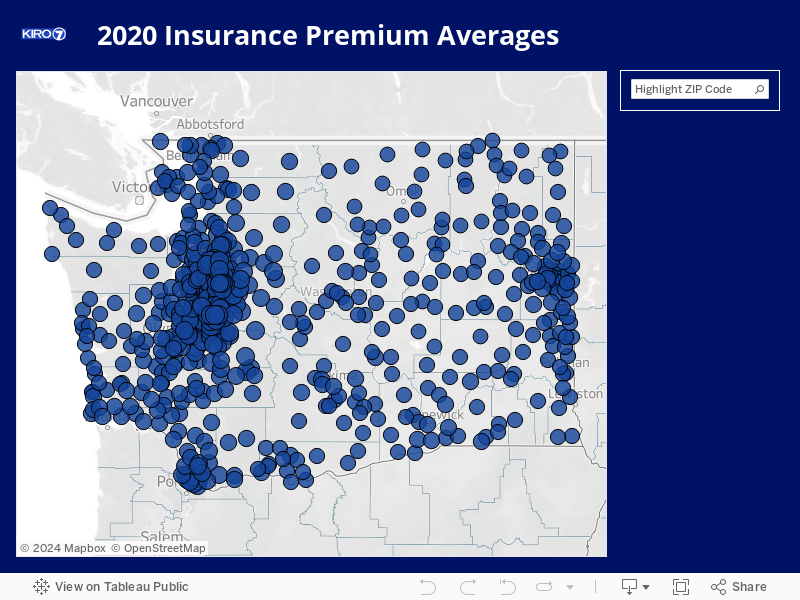

See how credit score affects average insurance rates in your area with this map.

See more of our reporting on insurance and gender here.

And follow our reporting on this legislation here:

- Governor speaks out in support of ban on use of credit scores to set insurance rates

- Insurance industry helped write changes that regulator says ‘gutted’ bill to take credit scoring out of insurance

- Bill to end use of credit scoring in insurance rates may get a vote - with major changes

- Race, credit scoring, and the most expensive neighborhood for car insurance in Washington

- Could you pay less for insurance, under a proposal to ban using credit scores to calculate premiums?

Email Jesse right now at consumer@kiro7.com

Cox Media Group