Olympia, WA — Senate Bill 5010 was written to end the use of credit scores to help determine insurance rates.

State Senator Mark Mullet (D-Issaquah), who’s the chairman of the Committee on Business, Financial Services & Trade, determines if the bill gets a vote. And he has pushed for amendments to the bill.

Mullet says the amendments say insurance companies can only weigh credit scores at no more than 50 percent to determine pricing. Right now, some companies use credit scoring as up to 60 percent of the rate factor.

And, starting in July, credit scores will freeze and cannot go down for insurance purposes for 18 months.

“So it just limits so they have to use other factors outside of your credit when determining your insurance premiums,” says Mullet.

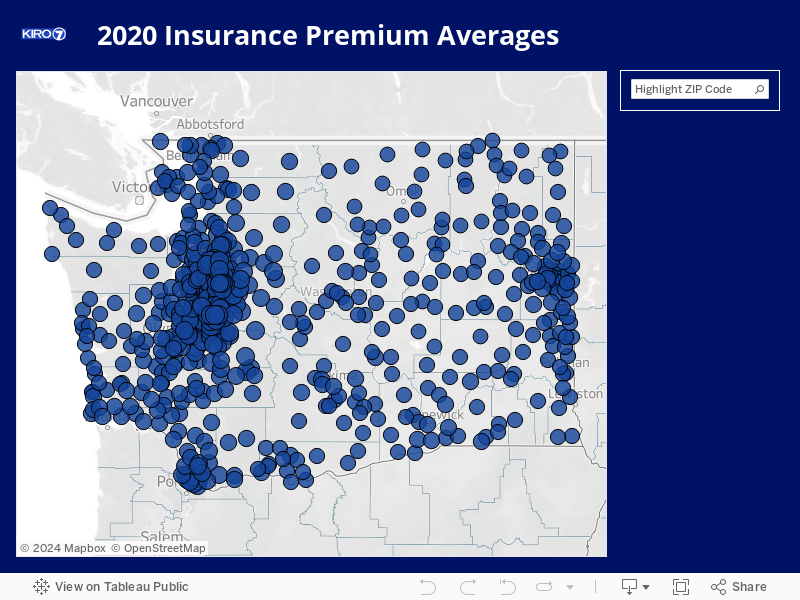

We’ve been investigating the use of credit scoring to determine insurance rates for months. We crunched numbers from a study on insurance rates in Washington provided by the Consumer Federation of America and found that in some cases, good drivers with poor credit can pay up to 79 percent more than those with the same record and excellent credit.

See the differences by zip code and credit score in our insurance map.

Insurance Commissioner Mike Kreidler says the practice hurts communities of color because they make up a higher percentage of low-income communities.

And, when we looked at U.S. census data, what we found in many cases is that the zip codes with the highest percentages of blacks also had the highest insurance rates in the state.

“But as a result of charging them more because they’re lower income, they have a disparate impact on people of color,” said Kreidler. “That’s a fact.”

When I asked him - do you believe the use of credit scoring for insurance rates is racist? He said:

“Yeah, I do.”

But Mullet says he wanted to amend the bill because he says senior citizens with good credit would get hurt if the bill passed.

“You have a lot of senior citizens on fixed incomes who are paying their bills and they have a long history of paying their bills so their credit score is really high,” says Mullet. “They would be hit negatively if the original form of the bill had passed.”

But Cathy MacCaul, advocacy director for AARP of Washington, says she is for the bill in its original form..

“And in the case of many seniors, they have - no longer have credit. They don’t have revolving credit on credit cards or they pay them off or they rely solely on a debit card which does not impact your credit rating. Or they’ve paid off their mortgage and are no longer holding a mortgage. And a credit score reflects your payment history,” says MacCaul.

We’ve heard from some seniors directly about this too. 70-year-old Deborah Anderson, of Port Angeles, is one of them.

She says she’s had rate increases because of a credit decrease, even with what she says is a perfect driving record.

“I would like to see the elimination of a requirement for a credit report. Because it affects me. Because it affects a good amount of people - seniors,” says Anderson.

I called Insurance Commissioner Mike Kreidler to ask what he thinks of the changes. Here’s his response:

“The substitute proposal from Senator Mullet is insufficient to help people who are struggling to make ends meet and maintains the insurance industry’s power. Making the use of credit scoring a little less harmful for a short period of time fails to offer real protection. “

See more of our reporting on insurance and credit score here and here, along with a report on price differences by gender here.

Email Jesse right now at consumer@kiro7.com

Cox Media Group